Content

During year-end closing, https://www.bookstime.com/s are liquidated and encumbrance account balances are returned to the unappropriated fund balance. Salaries and benefits make up an important part of encumbered funds, suggests the cloud spend management system Purchase Control. A company must pay its employees regular wages and provide promised benefits such as health insurance. If a company plans to do more hiring, it must increase the amount encumbered for salaries.

What is an encumbrance on property ownership?

Any burden, interest, right or claim which adversely affects the use of, or the ability to transfer, property. Sometimes the term is used more narrowly to refer just to security interests or similar arrangements affecting property.

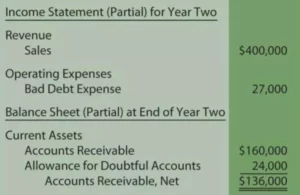

Encumbrances reserve a portion of an appropriation representing an obligation that has not been paid, or commitments related to unperformed contracts for goods and services. Outstanding encumbrances are the recognition of commitments related to unfulfilled purchase orders or outstanding contracts which will subsequently be recognized as expenditures when goods and services are received. In government accounting, for instance, encumbrances are leveled against the relevant appropriation account and are often used when there are multi-year contracts in place.

Why Is Encumbrance Accounting Important?

An encumbrance can impact the transferability of the property and restrict its free use until the encumbrance is lifted. The most common types of encumbrance apply to real estate; these include mortgages, easements, and property tax liens. Not all forms of encumbrance are financial, easements being an example of non-financial encumbrances. An encumbrance can also apply to personal – as opposed to real – property.

- While the new government-wide statements are prepared on the full accrual basis, accounting and budgeting for governmental funds are still on modified accrual.

- After the vendor accepts the purchase order and delivers the goods or services, the purchasing organization becomes liable to make the payment.

- With encumbrance accounting, future payment obligations are recorded in financial documents as projected expenses.

- The number represents a limit; if the company spends more, then it has gone over budget.

Encumbrance accounting primarily allows nonprofits and government organizations to record and monitor all future and planned expenses. Encumbrance accounting acts as a budgeting tool, resulting in more effective planning, allocating, and controlling their budgets. With encumbrance accounting, organizations record anticipated expenditures beforehand. This encourages transparency and increased visibility in how the budget is being allocated and how money is being spent. As a result, organizations can track their expenditures against the allocated budget more effectively. The purchasing company spends the encumbered amounts after confirming vendor invoices referring to the purchase order.

What is an Encumbrance?

They are encumbrance accountinged and depreciated in the government-wide statements, not in individual funds. A specific consequence of not reporting in the new model is that an auditor may not issue an unqualified opinion on financial statements not prepared in accordance with GAAP.

- Encumbrance accounting has many benefits for a company, including better visibility, improved expenditure control, and more precise analysis.

- When you record encumbrance within your ledger, it makes budget data much more accessible.

- Enable digital transformation and drive strategy with all your financial processes and data in a unified platform — owned by Finance.

- Money from the encumbrance account is moved into the appropriate account to pay the invoice, and accounts payable handles the vendor payment.

While appropriations are money set aside for budgetary line items, encumbrances are reserves for a specific item. Some examples of encumbrances are utility payments, tax payments, and payroll. Encumbrances are not considered actual expenses and are not included in actual-expense balances. With Encumbrances, no payments leave the University and no actual expense would be generated on a ledger, since it is an expectation of a future actual transaction. Appropriations represent legal spending limits prescribed by the entity’s governing body. Appropriations are usually established for departmental units and/or for various types of expenditures (salaries, equipment, supplies, etc.).

The Advantages of a Budget Within a Project

The American Institute of Certified Public Accountants has advised that statements not prepared according to the provisions of GASB 34 normally should result in an adverse opinion. The California Department of Education has modified its financial reporting software to help LEAs prepare the new statements on the full accrual basis. An available appropriation represents the amount of the appropriation that can still be obligated or spent within the availability period allow in the Budget Act. The available appropriation is determined by subtracting actual expenditures and outstanding commitments from the appropriated amount. Unless the unobligated appropriation balance is specifically reappropriated for a new term, it cannot be encumbered after the end of the appropriation term. All unobligated appropriation balances must be lapsed by processing a budget lapse transaction into USAS. The Comptroller’s office automatically lapses all unobligated balances as early as Nov. 1 each year.